As tax season approaches, a common question arises for those who maximize credit card rewards: are those perks taxable income? The reassuring answer, for most, is no. The vast majority of rewards earned through everyday spending aren't subject to taxes.

The key lies in the effort required to earn those rewards. When you spend money to accumulate points or miles, the IRS generally views those rewards as rebates – a discount on purchases you would have made anyway. This means your standard spending isn’t considered taxable income.

However, there’s a crucial exception. Rewards received *without* a corresponding purchase – like referral bonuses or automatic sign-up bonuses for opening a new bank account – are considered taxable income. These are essentially gifts, not discounts, and are treated accordingly by the IRS.

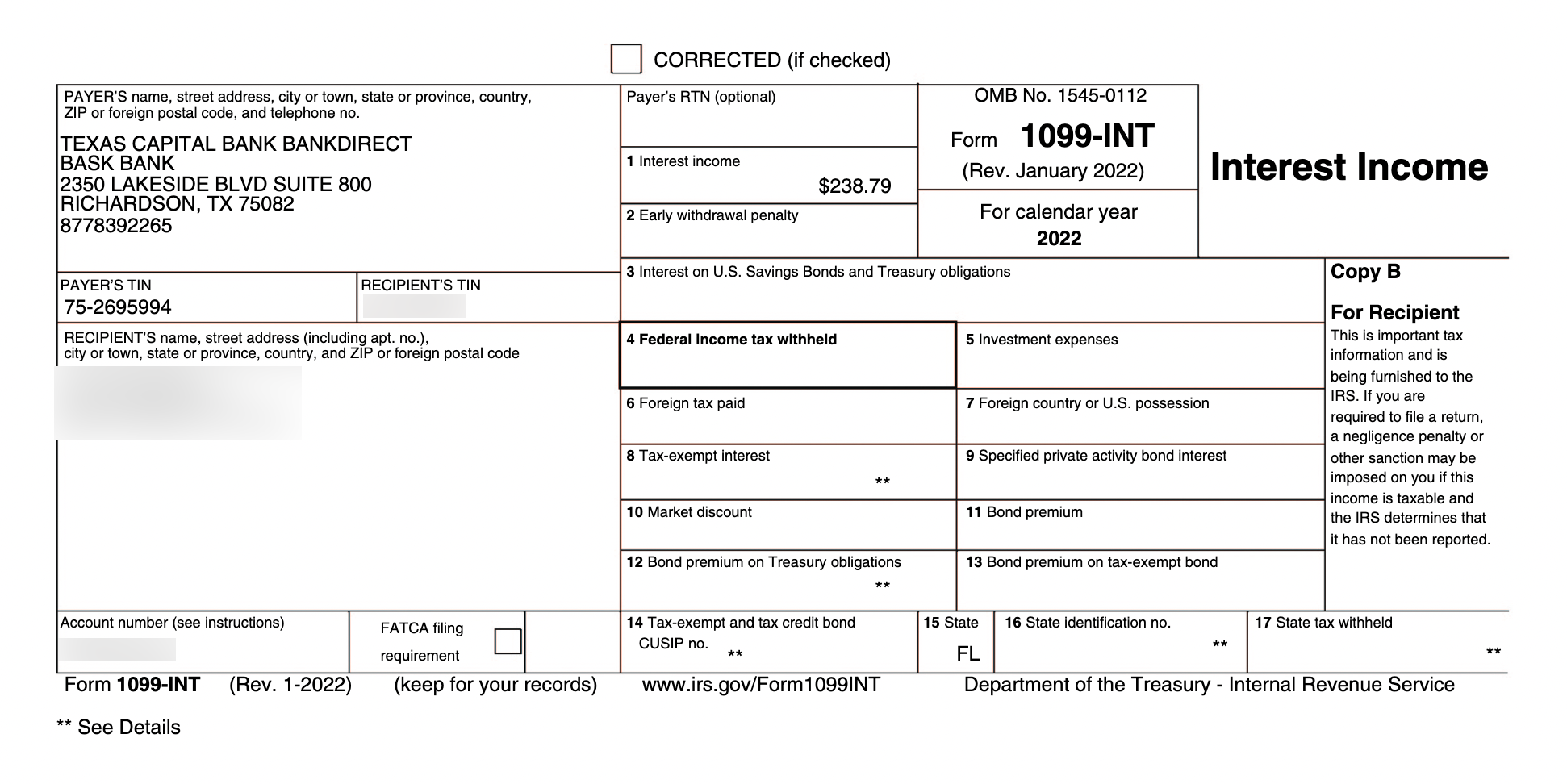

If you’ve been actively referring friends or opening new bank accounts solely for the bonus, be prepared. You might receive a 1099 form detailing this income. Even if you don’t receive one, the responsibility to report this income remains with you.

Specifically, referral bonuses trigger this tax implication. Because you earn the bonus without spending, it’s classified as income. The person *you* referred, however, won’t face taxes on their bonus earned through meeting spending requirements.

Cash back rewards earned through regular spending are generally safe from taxation, thanks to a 2010 IRS memorandum. But, like other bonuses, cash back received for simply opening an account without a spending requirement is taxable.

The same principles apply to business credit cards. Rewards earned on purchases aren’t taxable, but welcome bonuses and referral bonuses are. When claiming business expenses, remember to deduct only the net cost after applying any statement credits.

Bank account welcome bonuses fall squarely into the taxable income category. Similar to credit card referral bonuses, these are earned without requiring spending. One individual recently received 1099 forms for bonuses from SoFi and American Express checking accounts.

What about the 1099 form itself? It’s an information return, sent to both you and the IRS, detailing income received from a third party. While not all issuers are required to send one if the amount is under $600, you are still obligated to report all taxable income.

Major issuers typically send 1099s for referral bonuses exceeding $600. If you anticipate receiving one and it doesn’t arrive, you can request it or estimate the income. Accurate record-keeping is essential, even without a 1099.

If you receive a 1099 in error, contact the issuer for clarification or correction. Historically, banks haven’t issued 1099s for statement credits, treating them as rebates, but this could change, so vigilance is key.

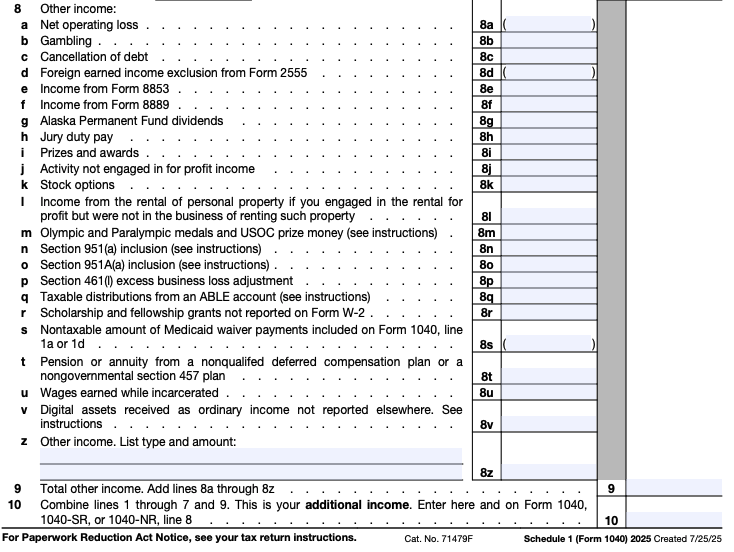

Where do you report this income on your tax return? Include it under “Other income” on line 8z of your 1040 form, using Schedule 1. Determining the value of points or miles can be tricky; use the issuer’s valuation or a reputable third-party assessment.

In conclusion, while the vast majority of credit card rewards are tax-free, bonuses earned without spending are taxable. Maintain meticulous records of your income sources, and remember that you’re responsible for reporting it, even if a 1099 isn’t issued. When in doubt, consult a tax professional.